Your ₹150 Coffee Is Not the Problem But Your ₹30 Lakh Car Decision Might Be.

A few years ago, when I was living in Chicago, a junior at my firm bought an Audi RS5. That car is one of my all-time favourites. Black, fast, completely ridiculous in the best possible way. I knew what he earned. I also knew what that purchase meant for his savings rate for the next five years. He was driving my dream car. I was driving a Toyota.

That moment stays with me because it was the clearest picture I have seen of how wealth is actually built and destroyed. Not through ₹150 coffees, but through the big decisions people make once or twice a decade. The ones that reshape their cash flows for years and carry real compounding weight.

This is not a story about being frugal. It is a story about where your financial leverage actually lives.

India's coffee shop market grew 12.7% in the last 12 months. Nearly 93% of cafe customers are between 18 and 45. The average spend per visit has crossed ₹660. And yet the most common piece of personal finance advice aimed at this same demographic is still some version of: stop buying coffee.

That advice is not wrong. But it is not the most useful thing you could do with your money. And that difference matters more than most people realise.

What the Latte Factor Actually Claims

The latte factor is a concept coined by American financial author David Bach in 1999. The idea is simple: small daily expenses, compounded over decades, add up to extraordinary sums. Skip the daily coffee, invest the savings, and watch time and compounding do their work.

The maths is real. We ran it on Indian numbers.

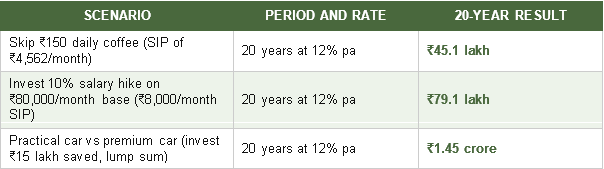

₹150 per day, every day, invested as a monthly SIP of ₹4,562 at 12% annual returns (the approximate long-term CAGR of the Nifty 50), over 20 years, grows to approximately ₹45.1 lakh.

That is not a small number. Most Indians never accumulate ₹45 lakh in their lifetimes.

But here is where personal finance advice tends to stop. It shows you the ₹45 lakh and implies you have found your path to wealth. What it does not tell you is what ₹45 lakh compares to when you look at the other financial levers sitting right in front of you.

The Calculation That Changes Everything

Run all three scenarios side by side and the picture shifts fast.

Formula used: SIP Future Value = PMT x [((1 + r)^n - 1) / r], where r = monthly return rate (12% / 12 = 1%), n = number of months. Lump sum: FV = PV x (1 + r)^n. Nifty 50 at 12% pa is a long-term historical CAGR assumption only. Past returns do not guarantee future performance.

A single 10% salary hike, fully invested, generates 1.75 times more than skipping your daily coffee for two decades. One car purchase decision, where you choose a practical option over a premium one and invest the difference, generates 3.2 times more. And these examples are conservative. Swap a premium apartment for a reasonably priced one, or stop upgrading your phone on EMI every two years, and the leverage compounds further still.

The coffee is not the problem. The coffee is simply the most visible thing.

What Personal Finance Advice Gets Wrong

The latte factor took off as a concept because it is genuinely comforting. It tells you that wealth is something you can access through discipline you can start today, with no special skills, no raise, and no difficult conversation with your manager. You just need to skip the beverage.

That framing is misleading for two reasons.

- First, it redirects your attention from high-leverage decisions to low-leverage ones. The energy spent tracking ₹150 coffees would deliver better returns if aimed at understanding your compensation, negotiating better, or building a skill that increases your income.

- Second, it creates the illusion of financial action without financial progress. Someone who gives up their daily coffee and feels virtuous about it, but has not addressed their savings rate on big purchases, is working harder than necessary for results that will significantly underperform.

Research from HelloWallet found that reducing small purchases had minimal impact on retirement readiness compared to the big variables: income growth, housing cost decisions, and consistent investment rate. Those three factors explained almost all of the variance in outcomes.

India adds another dimension to this. With median urban salaries in the ₹30,000 to ₹50,000 per month range, and cafe visits averaging ₹660 per person, coffee is not the largest discretionary line item for most Indians. The phone upgrade cycle, the car loan EMI, the annual international trip on a credit card at 36% interest, these are the financial decisions where wealth accumulates or disappears, silently and at scale.

So Does the Daily Coffee Actually Matter at All?

Yes. Just not in the way it is usually framed.

Tracking small expenses matters because it builds financial awareness. If you genuinely do not know where your money goes at the end of each month, logging your coffee spend is a useful starting point. Not because ₹150 will change your life, but because the discipline of tracking one thing tends to expand into tracking everything else.

The problem is when the awareness becomes the goal. When 'I gave up my coffee' becomes the identity rather than the first step toward a broader understanding of where your income goes and where it could go instead.

Give up the coffee if you want to. But do not stop there and call it a financial plan.

The Three Levers That Actually Build Wealth

If you want to make a real difference to your financial future, these are the areas where your attention pays off.

- Your income growth rate. Whether through salary negotiations, role changes, a side income stream, or building a high-value skill, the amount coming in is still the single largest lever in any personal finance equation. A 10% hike on ₹80,000 per month, invested fully for 20 years, generates ₹79 lakh. No coffee sacrifice required.

- Your big purchase decisions. Cars, phones, apartments, international holidays paid by credit. These are the decisions that lock your cash flow for months or years at a time. The difference between a thoughtful and an impulsive call on a ₹20 lakh to ₹30 lakh purchase is worth far more than any number of skipped coffees.

- Your investment rate on whatever you do save. Consistency and time in market are the real compounding engines. A SIP of ₹5,000 per month for 20 years at 12% grows to roughly ₹49 lakh. The same ₹5,000 sitting in a savings account at 3.5% grows to about ₹88,000 over the same period. The gap is not in the amount. It is in where the money is placed.

The coffee is a rounding error. Focus on the spreadsheet.

What is one big purchase decision you made in the last two years that you wish had gone differently? Not the ₹150 one. The ₹15 lakh one. Drop in a note or tell me in the comments of our video post launch tomorrow.