The Money-Happiness Equation: What Research Says (And What Wealthy Indians Regret)

In March 2026, the World Happiness Report was released. India ranked 116th. Out of 146 countries.

Let that sit for a second. One of the fastest-growing economies in the world. Record mutual fund inflows. A stock market that has compounded at double-digit returns for over a decade. A middle class that is larger and richer than at any point in Indian history. And we are 116th on the global happiness rankings, behind Bolivia, Kosovo, and Serbia.

The headline got a few shares on LinkedIn, sparked the usual debate about whether the methodology is biased against developing nations, and then disappeared from the feed. But if you actually sit with that number rather than dismissing it, it raises a question worth taking seriously: at what income level does earning more actually stop improving your life?

Researchers have been trying to answer that question for decades. In 2010, Nobel laureate Daniel Kahneman published a study suggesting that beyond $75,000 a year, more income did not improve day-to-day emotional wellbeing for American households. That number got quoted in every personal finance article for the next decade. Then in 2021, a researcher at Penn named Matthew Killingsworth challenged it with a much larger dataset and found that wellbeing actually keeps rising with income above that threshold. The two of them sat down together in 2023 and ran a new adversarial study to resolve the disagreement. The updated finding: the plateau is real, but it lands somewhere between $175,000 and $250,000 a year. Adjusted for purchasing power in India, that translates to roughly ₹20 to 30 lakh per year for a household in a major city.

Here is the nuance that did not make the headlines. It is not that money stops mattering entirely after that point. It is that what money does for you changes. Below a certain level, income buys basic security, food, health, and education. Above it, additional income mainly buys time, freedom, and the ability to say no. Those last three things have a different relationship with your income number than the first set do.

I have been thinking about this for longer than I expected to. Before returning to India in 2023, I spent eleven years in investment banking, most of it at Deutsche Bank, with time in Mumbai, Chicago, and London. By the time I left, I was well past any earnings threshold that research would associate with happiness. And in 2021, while I was in Chicago with a US visa, my uncle and my grandmother both passed away during COVID. I could not travel. Income was not the relevant variable that year. Not even slightly.

That gap between what money can and cannot buy is what this article is actually about.

What the Research Is Actually Telling You

The Kahneman-Killingsworth collaboration landed on a finding that most coverage missed. The plateau does not happen at the same income level for everyone. For people who are already reasonably happy, money keeps improving wellbeing as income rises, even at high levels. For people who are chronically unhappy, the income effect flattens out much earlier. The unhappiest 20 percent of their sample showed a clear saturation effect. The happiest 20 percent showed almost none.

What this means practically: if you are structuring your financial life around chasing a higher salary and you are not happy at your current level, the research suggests more money will help somewhat, but it will not solve the underlying problem. On the other hand, if you have a solid baseline of wellbeing and a clear sense of what you are investing toward, income growth keeps compounding into life satisfaction in a meaningful way.

The study also showed something that gets almost no attention: the emotional quality of your daily experience matters more than your overall life evaluation score. You can earn ₹3 lakh a month and report that your life is going well while still having miserable Mondays. Those are two different things, and the research measures both of them separately.

Why India's 116th Ranking Is More Interesting Than It Looks

The World Happiness Report does not just measure income. It scores six variables: GDP per capita, social support, healthy life expectancy, freedom of life choice, generosity, and perceptions of corruption. India's income per capita has been climbing steadily. The other five have not moved in the same direction.

The happiest states in India in 2026, according to domestic research by HappyPlus Consulting, are Himachal Pradesh and Mizoram. Not Maharashtra. Not Karnataka. Not Delhi. These are smaller states with tighter community structures, slower city rhythms, and measurably better air quality. Their per capita incomes are nowhere near Bengaluru or Mumbai. Their residents consistently report higher life satisfaction scores than metro dwellers who earn multiples of their income.

This is not sentimentality about simple rural life. It is data. And it tells you that the income-happiness relationship in India has substantial noise from other variables: air quality, commute times, family proximity, community ties, and the degree to which the systems around you actually function. Some of those variables are addressable with money (you can afford to live closer to work, pay for better healthcare, access cleaner environments). But income does not create them. It only provides access.

This distinction matters enormously for how you build a financial plan.

Your Enough Number (With the Maths)

Here is the practical question that all of this leads to. If you were designing your financial life around a specific target rather than a vague notion of "more," what would that target actually look like?

For most urban working Indians, "enough" has four components: a home that you own or are on a clear path to owning, no high-interest consumer debt, a year of expenses in accessible liquid savings, and a corpus large enough to generate passive income that covers your monthly expenses comfortably.

Let us focus on that last one, because it is the number most people have never actually calculated.

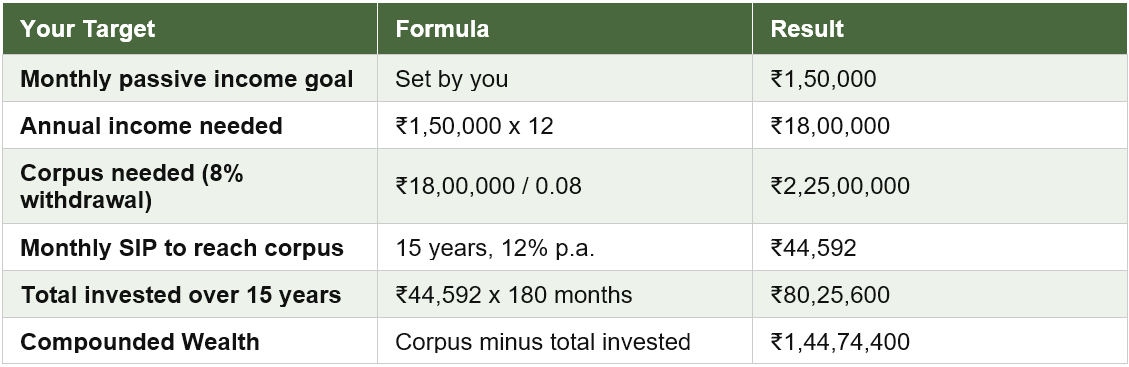

Assume your target monthly passive income is ₹1.5 lakh. That is a reasonable figure for a family in a metro city with EMIs sorted, school fees, household costs, and a lifestyle that includes occasional travel and eating out. Using a sustainable 8 percent annual withdrawal rate, the corpus needed to generate that income without touching the principal looks like this:

₹44,592 per month. That is your number if your happiness target is ₹1.5 lakh a month in passive income and you have 15 years to get there. It is specific. It is trackable. It is very different from investing whatever is left over after expenses and hoping for the best.

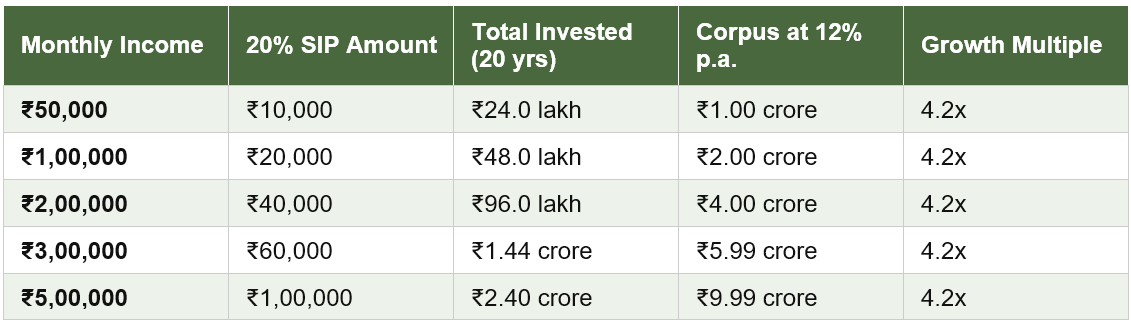

Now look at what happens when you apply a consistent 20 percent savings rate across different income levels:

The growth multiple is 4.2x regardless of income level. That is the point. Your income level determines the size of your corpus, but your savings rate determines whether you get there at all. A person earning ₹50,000 a month and saving 20 percent will build more than a person earning ₹3 lakh a month and saving 5 percent. Consistently.

What High-Income Indians Say They Regret

I have not run a formal survey on this, but the pattern in conversations with people who have crossed what should be their enough threshold is consistent. The regrets are almost never about money. They are about the choices money was supposed to buy but never did.

Three come up repeatedly. The first is lifestyle inflation that locked in a cost base they could not step back from. The flat upgrade, the premium school fees, the overseas holiday that became an annual fixture. Each increment felt reasonable in isolation. As a system, it eliminated the freedom that the income was supposed to create.

The second is missing the compounding window. People who earn well but begin investing seriously only in their late 30s. The habit that should have started in the first paycheck did not start until a financial crisis or a conversation made it impossible to ignore. The cost of that delay, as the SIP table above shows, is measured in crores over a 20-year period.

The third is the identity trap. When your income becomes the primary signal of your worth, stepping off the treadmill becomes psychologically impossible even if it is financially viable. The promotion, the designation, the salary band are no longer things you earn. They become things you need, for reasons that have nothing to do with what the money actually buys.

The Financial Plan That Takes This Seriously

Here is the reframe that I keep coming back to. Your enough number is not a ceiling on your ambition. It is a floor for your security.

Know precisely what it costs to run your life well. Not the life you think you should be living, the one you actually enjoy and find meaningful. Add the budget for the things that genuinely matter to you: travel, health, time with family, education, experiences worth paying for. Subtract the items you have been buying primarily to signal a certain kind of success.

The gap between those two figures is your investment number. Not vaguely, not when there is something left over. Monthly, automated, in a SIP that runs whether or not you are paying attention.

The goal of this plan is not to get rich in some abstract sense. It is to reach the point where you can choose. Choose to step back from a job that stopped being interesting three years ago. Choose to take a year and build something. Choose to be home for the things that matter before you run out of the years when they do.

Thursday's video at 7 PM IST does the full walkthrough: how to calculate your personal enough number, what a realistic SIP plan to reach it looks like at different income levels, and the one number that makes the most difference if you are starting today. Come with your actual monthly expenses written down. You will use them.