A 10-Year Financial Roadmap for Indians Who Feel Like They're Starting Late

In December 2025, PGIM India published the third edition of its Retirement Readiness Report. They surveyed over 3,000 adults across the country. The headline finding should have stopped every working Indian in their tracks.

Only 37% of Indian households had a retirement plan. Two years earlier, that number was 67%. In 24 months, the share of Indians actively planning for their financial future had almost halved.

What made it worse was that this was not happening because people stopped caring. Retirement came out as the top financial priority. People cared deeply. They just were not acting. And when the researchers dug into the reasons, one answer kept surfacing. They felt like they had left it too late.

That belief -- that the window has closed -- is the most expensive financial story most Indians will ever tell themselves.

I understand where it comes from. When I left Deutsche Bank in 2023 at 34, after eleven years in investment banking and advising on over USD 13 billion of transactions, I was walking away from a VP-to-MD trajectory. From the outside, some people thought I was starting from zero. What they did not see was the 10-year plan that made the leap possible. Not a vague aspiration. A specific roadmap: what I needed in savings before I could make the jump, what the first three years would look like, what I was building toward by year ten. That clarity is what made an intimidating decision executable.

This article is for everyone who has convinced themselves that they missed their window. Whether you are 30 and feel like you should have started at 22, 35 and watching colleagues who invested earlier, or 40 and quietly wondering if 20 years is even enough. Here is what the math actually says, and here is a 10-year plan that works wherever you are starting from.

The Number That Should Alarm Every Indian Under 50

The PGIM India data tells a story that goes beyond one headline statistic. The 37% figure is striking, but the reasons behind it are more instructive.

46% of respondents reported significant financial stress in 2025, up from 32% two years earlier. Rising costs, EMIs, school fees, rent -- these were pushing day-to-day survival higher on the priority list than long-term planning. 42% expected to rely on their children or relatives in retirement. And 32% were making financial decisions based on social media advice they had never verified with anyone qualified.

Here is the part that rarely gets said: the people caught in this situation are not financially careless. Most are working hard, managing real pressures, and making reasonable choices month to month. The problem is not character. It is the absence of a plan that accounts for compounding.

Because compounding does not care how hard you work. It only cares how long your money has been in the market.

What Starting Late Actually Costs You (The Honest Numbers)

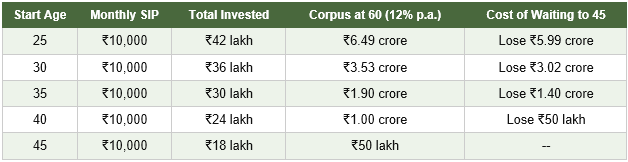

Here is the comparison that matters most. Five different starting ages. Same ₹10,000 monthly SIP. Same 12% annual return assumption, which is roughly the Nifty 50's long-term historical CAGR. Target retirement age: 60.

The numbers are real, and the cost of delay is real. Starting at 25 versus 35 costs you over ₹3.0 crore on the same ₹10,000 monthly SIP.

But here is what the fear narrative gets wrong: every row in that table is still a meaningful outcome. ₹1 crore by 60 starting at 40. ₹1.90 crore starting at 35. These are not failure numbers. They are starting points, and they only hold if you invest a flat ₹10,000 forever. Almost nobody does that. And that brings us to the part most people miss.

The Three-Phase 10-Year Roadmap

A 10-year financial plan is not a spreadsheet you build once. It is a progression. The people who actually execute it do not try to do everything at once. They move through phases, each one building the capacity for the next.

Here is how to think about it, regardless of whether you are starting at 30, 35, or 40.

Phase 1 (Year 1 to 3): Build the Foundation

Before any investment conversation, three things need to be in place. A 6-month emergency fund in a liquid fund or high-yield savings account. Term life insurance covering at least 15 to 20 times your annual income. Health insurance with a sum assured that actually covers hospitalisation costs in a private hospital in your city.

These are not optional. They are the floor. Without them, a single medical emergency or job loss can unravel every SIP you have started. Once the floor is in place, start your SIP. Even ₹5,000 a month is a real start. The number matters less than the habit and the timeline.

Phase 2 (Year 4 to 7): Accelerate

By year 4, your income should be higher than it was in year 1. Most people let lifestyle inflation absorb the entire increment. The move that separates wealth builders from everyone else is routing at least half of every meaningful salary hike into the SIP.

This is also when the step-up SIP becomes your most powerful tool. Phase 2 is also when you start thinking about asset allocation beyond equity: index funds as the core, with PPF, NPS, and debt instruments playing supporting roles depending on your timeline and risk profile.

Phase 3 (Year 8 to 10): Optimise and Lock In

By year 8, your corpus has enough mass that the compounding engine is doing serious work. This is when you review everything. Are the funds still performing relative to benchmarks? Is the asset allocation still right for your horizon? Have your tax liabilities changed?

This is also when goal-based thinking becomes specific. Retirement corpus, children's education, property. Each goal has its own horizon and its own instrument. Phase 3 is where you match them properly.

One Move That Changes Everything: The Step-Up SIP

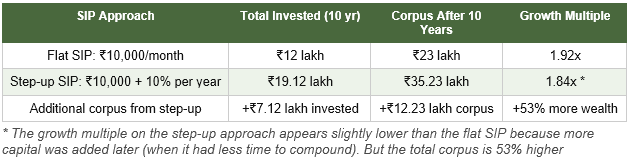

Most people think of SIPs as fixed amounts. ₹10,000 a month, every month, for 10 years. That approach works. But there is a version that works significantly better, and it costs less in the early years when cash flow is tightest.

The step-up SIP: you increase your monthly investment by 10% every year, roughly matching an average salary increment. Here is what the same ₹10,000 starting SIP looks like over 10 years, flat versus stepped up.

₹12.23 lakh more in your corpus from the same starting amount. That is the difference between a flat and a step-up SIP over a single decade. The reason it works is that each rupee you add in the early years gets more compounding time than the rupee you add in year 10.

The practical implementation: when you set up your SIP on Zerodha, Groww, or your platform of choice, set a calendar reminder every April 1 to increase the amount by 10%. Some platforms now support automatic step-up. Either way, the habit is identical.

What to Do This Week

A 10-year plan starts with a short list of immediate actions. Not a full financial overhaul. Not a portfolio review. Just these five things.

- Calculate your actual net worth today. Assets minus liabilities. Be honest. This is your starting point, not a judgment.

- Check your insurance. Do you have term life? Does your health cover what hospitalisation actually costs today? Fix these before you invest another rupee.

- Check your emergency fund. Six months of expenses in a liquid fund or high-yield savings account. Build this before you accelerate your SIP.

- Start or increase your SIP by one step. Not the perfect amount. One step up from where you are now. ₹5,000 if you have nothing. ₹15,000 if you are at ₹10,000.

- Set a step-up reminder. Next April 1. Increase your SIP by 10%. Put it in your calendar right now.

The most common response to all of this is: I need to think about it. That thinking has a cost. The table above shows you exactly what it is, measured in lakh, per decade.

Thursday's video goes deeper into the real cost of the financial decisions we postpone. Come with your calculator.

What age did you start investing, and what do you wish you had known earlier? Tell me in the comments. The most useful thing I can do with your answer is build the next article around it.