The Rs 1 Lakh Savings Experiment: What Happens When You Get Obsessively Specific

There is a line in the RBI's 2023-24 Annual Report that most people skipped right past. India's household financial savings rate fell to 5.1% of gross national disposable income. That is the lowest level in 47 years.

We are earning more than any previous generation of Indians. Our salaries are higher, our career options wider, our access to investment products better than they have ever been. And yet, as a country, we are saving less of what we earn than at almost any point in living memory.

The usual explanations are rising EMIs, lifestyle inflation, cost of living in cities. All of those are real. But there is another culprit that nobody talks about: savings advice that is too vague to follow.

"Save 20% of your salary." "Build a corpus." "Start early." Every piece of advice is correct in principle. None of it tells you what to do this month, on a specific date, in a specific account, with a specific rupee amount. And without that specificity, good intentions die quietly in the gap between knowing and doing.

I bought my first mutual fund in October 2012. Third month of earning a salary. I was 24 years old, working at Nomura in Mumbai, and I had been renting my accommodation. But I had already decided the exact amount I would invest. Not roughly. Exactly. I did not wait until I was settled. I did not wait until I felt financially comfortable. I picked a number, set up the SIP, and started. That decision to be obsessively specific about a small amount compounded over years into something much larger than the amount itself.

This article is about what happens when you run the same experiment: pick one specific number, set one specific timeline, and build one specific system. The number is Rs 1 lakh. The timeline is 12 months. The system takes about 20 minutes to set up.

The Problem With 'Save More' as a Strategy

Ask someone how much they saved last month and most people cannot tell you. Not because they do not want to save, but because saving is happening (or not happening) as whatever is left over after spending. This is the wrong order.

The "save what is left over" approach has a structural flaw: spending expands to fill available income. There is a very well-documented psychological tendency at work here. Lifestyle creep. The moment you get a raise, your reference point for what is normal shifts upward. So the leftover you were counting on quietly disappears.

The fix is not willpower. The fix is specificity. When the number is specific, the account is specific, and the date is specific, the decision is already made. You are not making a choice every month. The choice was made once, in advance, and the system runs it for you.

So what is the specific number? Let us run the actual experiment.

The Experiment: Rs 8,334 a Month for 12 Months

Target: Rs 1,00,000 in 12 months.

Formula: Simple division. Rs 1,00,000 divided by 12 months equals Rs 8,333.33. Round up to Rs 8,334 per month and by the end of 12 months you have set aside Rs 1,00,008. You have crossed the line.

That is the number. Rs 8,334. Not "around eight thousand". Not "whatever you can manage." Eight thousand three hundred and thirty-four rupees, transferred on the same date every month, the date when your salary hits your account, to a separate account.

Why does this work when vague savings advice does not? Because the specific number removes the decision from your monthly routine. You do not decide whether to save this month. The standing instruction does it for you. The mental load goes to zero once the system is in place.

Now, the obvious question: where do you put the money?

Where You Park the Money Also Matters

Rs 1 lakh in 12 months is the goal. The place you park your monthly Rs 8,334 determines whether you get exactly Rs 1 lakh at the end or a little more.

Here is the comparison across three options, calculated using the SIP future value formula (annuity due, monthly compounding):

All figures calculated via SIP future value formula (annuity due, payments at start of period). Savings account and liquid fund returns are approximate; actual returns will vary. Liquid mutual funds are not guaranteed instruments.

The difference between a current account and a liquid fund over 12 months is roughly Rs 3,874. That is not the point of the exercise. The point is that the discipline of the Rs 8,334 SIP matters far more than the return on a 12-month timeframe. Still, parking it in a liquid fund rather than an idle current account is a better habit to build and costs you nothing extra in effort.

A few platforms where this is straightforward: Zerodha Coin, Groww, Kuvera, and most bank apps now have liquid fund options available in a few taps. Set the instruction once. Let it run.

What Rs 1 Lakh Becomes When You Actually Invest It

Now here is the more important conversation. Saving Rs 1 lakh is step one. What matters more is what you do with it afterwards.

The goal of this savings experiment is not to accumulate idle cash. It is to build the habit of hitting a specific number on a specific timeline, so that when the money is ready, you move it immediately into a long-term investment. An index fund. A diversified equity mutual fund. Something that can compound over years, not months.

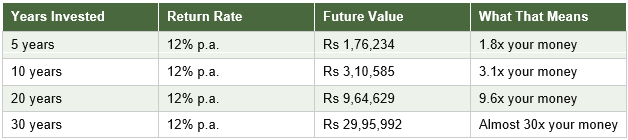

Here is what Rs 1 lakh looks like invested at 12% per annum, the approximate long-term historical CAGR of the Nifty 50:

Formula: FV = PV x (1 + r)^n. PV = Rs 1,00,000, r = 12% p.a., annual compounding. Nifty 50 historical CAGR is approximate; past returns do not guarantee future performance. Pre-tax, pre-expense.

Rs 1 lakh in 30 years at 12% becomes approximately Rs 30 lakh. That is the power of patience and a 12-month savings habit that you then leave alone.

The person who saves Rs 8,334 a month for 12 months and invests the lump sum at 25 ends up with roughly 30 lakh at 55. The person who waits until 35 to do this ends up with roughly 9.6 lakh at 55. The habit matters. The starting age matters. The specific number makes it possible to start.

The Three-Account System That Makes This Work

One account for everything is the fastest way to sabotage any savings plan. Money that shares a home with your daily spending will get spent. This is not a character flaw. It is just how humans are wired.

The setup I have used for years, and which I still run today for my own finances, is three separate accounts with three separate purposes:

Account one is for operating expenses. Salary comes in here. Rent, groceries, subscriptions, EMIs go out from here. This account runs the month.

Account two is for savings. Rs 8,334 moves here automatically on the 1st of each month. You do not touch this account during the month. At the end of 12 months, this is your Rs 1 lakh, ready to be invested.

Account three is your emergency buffer. Three to six months of expenses that you do not touch unless there is a genuine emergency. This is what gives you the psychological safety to keep your savings account intact even when things get tight.

The Rs 8,334 savings instruction should ideally go out before you can spend it. Many banks let you set a standing instruction for the 1st or 2nd of each month, right after your salary credit. Use that feature. Pay yourself first, then manage the rest.

This is not a revolutionary system. But it is the specific, operational version of "save more". And specific beats aspirational every single time.

Rs 8,334 a month. One standing instruction. Three accounts. That is the whole experiment. Try it for one year and tell me what you notice.

If you want to watch me walk through the actual maths, the three-account setup, and the next step once you have the Rs 1 lakh ready, that video goes live on the Invest with Vessify channel on Thursday 19th March at 7:00 PM IST.

And here is the question I want you to sit with: what is the specific savings target you have set for this year, and do you have a system that makes it automatic?

DISCLAIMER: All calculations are for educational purposes only and do not constitute investment advice.