The Procrastination Tax: How Rs 10,000 You Don't Invest Today Costs You Lakhs

When I was at Deutsche Bank for 10 years, I had no choice about how to invest. Compliance rules for investment bankers meant individual stocks were largely off the table. No picking winners. No waiting for the perfect entry point. My entire US savings went into ETFs and index funds, month after month, on a schedule, without drama.

At the time, it felt like a restriction. Looking back, it was the best thing that could have happened to my personal finances. The option to procrastinate was simply not available. And because I could not wait for the right time, I never paid the procrastination tax.

Most people do not have that forced discipline. They have the best intentions and a list of reasons to start next month. The market is too high right now. I will invest after I clear this loan. I need to understand it better first. I will start when I have more to invest.

Here is what those reasons actually cost, in rupees.

What the Procrastination Tax Actually Is

The idea behind the procrastination tax comes from one of the oldest and most well-established concepts in finance: time value of money. The principle is straightforward. A rupee today is worth more than a rupee tomorrow, because a rupee today has time to grow.

When you delay investing, you are not just postponing a financial action. You are handing back the one thing money cannot buy once it is gone: time in the market. And compounding, which is the engine behind every long-term investment return, needs time the way a plant needs water. Remove it, and the whole equation changes.

The procrastination tax is the measurable difference between what you would have had if you had started when you first thought about it, and what you actually end up with because you waited.

Let's Put a Number on It, Starting With a Single ₹10,000

Say you are 25 years old today. You have ₹10,000 sitting in your bank account. If you invest it right now in a Nifty 50 index fund and leave it there until you are 60, at a historical long-run return of 12% per year, that ₹10,000 becomes ₹5.28 lakh.

Now say you wait. Just one year. You invest the same ₹10,000 at 26 instead of 25. Same fund. Same 12%. How much do you lose?

₹56,571. Gone. From one year of inaction on one ₹10,000 note.

Wait five years and the procrastination tax on that same ₹10,000 is ₹2.28 lakh. Wait ten years and you have paid ₹3.58 lakh in procrastination tax on a single ₹10,000 investment that you never made.

That is not a typo. One decision to wait ten years on one ₹10,000 bill costs ₹3.58 lakh. Now scale that to a monthly SIP.

The Monthly SIP Version: This Is Where It Gets Uncomfortable

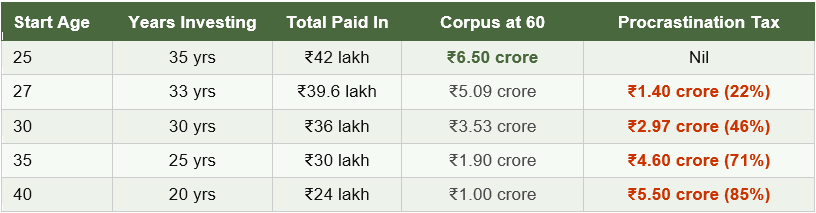

The lump sum example is instructive, but most people invest through SIPs. So let us look at what ₹10,000 per month costs you at different starting ages, with a retirement target of 60.

If you start a ₹10,000 SIP at 35 instead of 25, you do not just lose 10 years of contributions. You lose ₹4.60 crore. That is 71% of your potential retirement wealth. Gone. Not because the market crashed. Not because you picked the wrong fund. Simply because you waited.

And every single month of that wait has a specific price tag. For a ₹10,000 SIP from age 25, one month of delay costs ₹6.53 lakh at retirement. That is what the math says. That is the procrastination tax, billed monthly, silently, forever.

The Most Counterintuitive Number in Personal Finance

Here is the finding that tends to stop people mid-sentence when they first see it.

A 22-year-old who invests ₹5,000 per month and stops at 60 ends up with ₹4.67 crore. Total amount invested: ₹22.8 lakh.

A 35-year-old who invests ₹15,000 per month and also stops at 60 ends up with ₹2.85 crore. Total amount invested: ₹45 lakh.

The 35-year-old invested twice as much money. And ended up with ₹1.82 crore less.

This is not a trick. The math is straightforward. The early investor had 13 extra years for compounding to work. Those early years, when the corpus is small but time is long, do more work than all the later high-contribution years combined. That is the compounding asymmetry. And it is why the procrastination tax is so brutal: the years you lose at the beginning are the most valuable ones.

The Most Common Excuses, and What They Actually Cost

Almost everyone who delays investing does so for one of four reasons. Let us be honest about each.

The first is the market timing excuse: I am waiting for the market to come down before I invest. The problem with this reasoning is that it assumes you will know when the bottom is. You will not. Nobody does, consistently. And while you are waiting, you are paying the procrastination tax every single month.

The second is the knowledge excuse: I need to understand investing better before I start. This one is understandable but misapplied. A basic Nifty 50 index fund requires zero expertise to invest in. You do not need to understand derivatives, P/E ratios, or balance sheet analysis to start a SIP in an index fund. Start first. Learn while your money grows.

The third is the amount excuse: I do not have enough to make it worth investing yet. The entire point of this article is that the amount matters far less than the time. ₹1,000 a month started at 22 is worth more than ₹5,000 a month started at 35. Start with whatever you have.

The fourth is the debt excuse: I will invest once I have cleared my loan. This one needs nuance. High-interest debt such as credit card debt at 36% should be cleared first. But if you have a home loan at 8.5% or a car loan at 10%, and you are using it as a reason to delay equity investing at an expected 12%, you are doing the math backwards.

How to Stop Paying the Tax, Starting Today

The cure for the procrastination tax is not motivation. Motivation fades. The cure is automation.

Set up a SIP through Zerodha Coin, Groww, or any platform you already use. Pick a date two days after your salary credit. Set the SIP amount. And remove it from your decision-making entirely. When investing is automatic, procrastination is not an option. That is exactly the position Suraj was in during his Deutsche Bank years, and it is the single most effective financial system he has used.

Start with what is comfortable. Even ₹2,000 a month. The specific amount matters less today than the habit. You can step it up. What you cannot do is buy back the months you missed.

Thursday's video, The Procrastination Tax, walks through this in full detail with specific fund recommendations, step-up SIP strategies, and the exact calculation framework behind all the numbers above. If the math in this article made you uncomfortable, the video is going to be even more uncomfortable. And that is exactly the point.

One Question Before You Go

If someone had shown you this table five years ago, what would you have done differently?

Most people answer that question immediately. The real question is: what are you going to do about it today?

Drop your answer in the comments below. I read every single one.